masyarakat Poster Layanan Masyarakat: Pengertian, Contoh Lengkap & Cara Membuat yang Efektif rizal hadizan Jumat, 24 April 2026 Poster layanan masyarakat adalah salah satu media komunikasi visual yang paling sering kita jumpai di kehidupan sehari-hari — mulai dari ...

Psikologi 21 Contoh Bakat dan Minat dalam Kehidupan Sehari-Hari rizal hadizan Sabtu, 19 Juli 2025 Pernahkah Anda bertanya-tanya apa yang membuat Anda bersinar di tengah keramaian? Atau mengapa Anda begitu menikmati aktivitas tertentu tan...

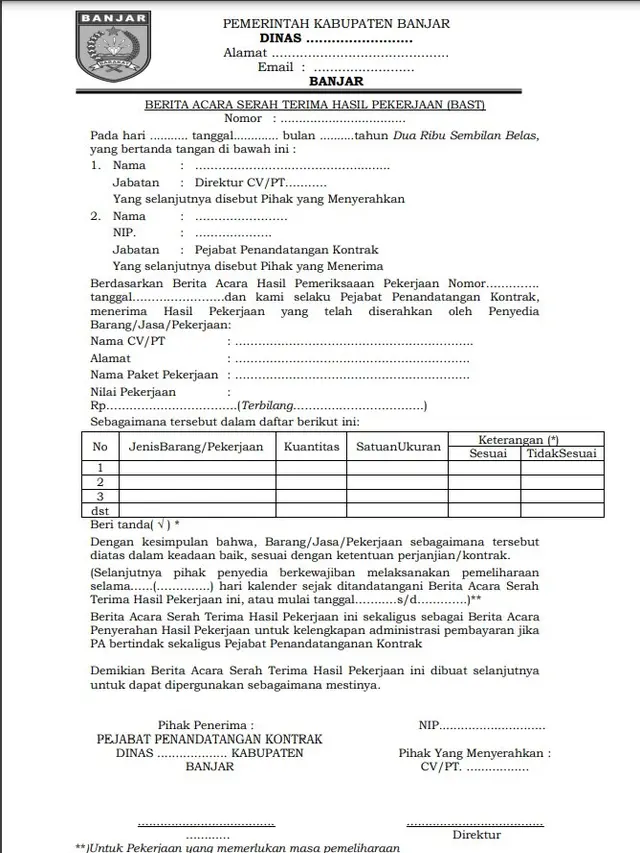

Bahasa Indonesia Contoh Berita Acara Lengkap dengan Format dan Cara Membuatnya rizal hadizan Berita acara adalah dokumen resmi yang digunakan untuk mencatat suatu peristiwa, kegiatan, atau transaksi secara formal. Dokumen ini memili...